Choppy Waters

After an amazing melt up since last November, the stock market has become choppy lately. When that happens, there is typically a ‘push-pull’ occurring that has the market uncertain of its next direction. In this case, the push higher is based on a growing economy and the presumably strong earnings that will bring. The pull downward is based on inflation data that is not as ideal as many expected and which may imply some resurgence of inflation. That, in turn, implies the rate cuts may not be as probable as they appear and even raises the specter of higher interest rates to come. Watch the S&P index and you can see which argument is holding sway on any given day. This week had plenty of news on both fronts, which defined the obvious chop this week. (Of course, this is all subject to change based on geopolitical issues too. The Middle East situation could expand quickly, if someone makes a mistake.)

Wednesday: CPI runs hot (i.e., higher than expected) for the third month in a row. When the inflation data came in higher than expected in January, it was attributed to the turn of the year adjustments in the data. The February increase was brushed off as ‘one of those things’, but when March data continued the trend, the bond market reacted strongly with interest rates rising and stocks took a dive.

Thursday: All is forgiven when PPI (Producer Price Index) data is slightly better than expected and the market rallies back.

Friday: Earnings reporting season begins with the banks, as usual. What was unusual, was the disappointing forecast laid out by JP Morgan as it reported excellent earnings. That sent the stock market tumbling back down.

We expect more of the same in the near term as key company earnings are reported and additional inflation data hits the wires. After a vey strong five-month rally, stocks are probably overdue for a breather anyway. If this is to turn into a larger correction, it will require rates to continue to drift higher and/or for first quarter earnings reports to disappoint.

Could Rates Continue to Drift Higher?

The chart below is the yield on the 10-Year Treasury Note from July 2023 to present (courtesy Yahoo! Finance). The bond market sure looks confused. From July into late October, we were in the ‘higher for longer’ narrative as the Fed remained steadfast that they were not close to lowering rates. As we turned into November, the bond market sniffed out that inflation numbers would continue to get better and rates quickly reversed course, punctuated by the December Fed announcement that they were consider rate cuts. By the way, this bond market rally was what prompted the massive run-up in stocks that we had the last several months.

At the end of 2023, everything changed again and rates reversed course yet again. The bond market was right once again, as January inflation numbers came in hot and that has pushed rates even higher. Looking at the chart, they don’t appear ready to reverse yet again. It will take some good news on the inflation front to move rates lower. If we don’t get it, we could easily revisit the 5% level. That would not be good for the stock market.

Could Earnings Disappoint?

We doubt earnings reports will disappoint in Q1. The economy has continued to grow and leading indicators remain low, but are improving. In addition, there is always some gamesmanship in earnings reports. Normally a quite high percentage of companies meet or exceed expectations each quarter as companies push analysts to appropriate levels well before the actual announcement. Much like the JPMorgan earnings results, the place where the rubber meets the road is when companies discuss expectations for the remainder of the year. From that perspective, there is a bit more risk in the Q1 earnings announcements, but even here, the economic backdrop is such that we don’t expect the JPMorgan announcement to be repeated often.

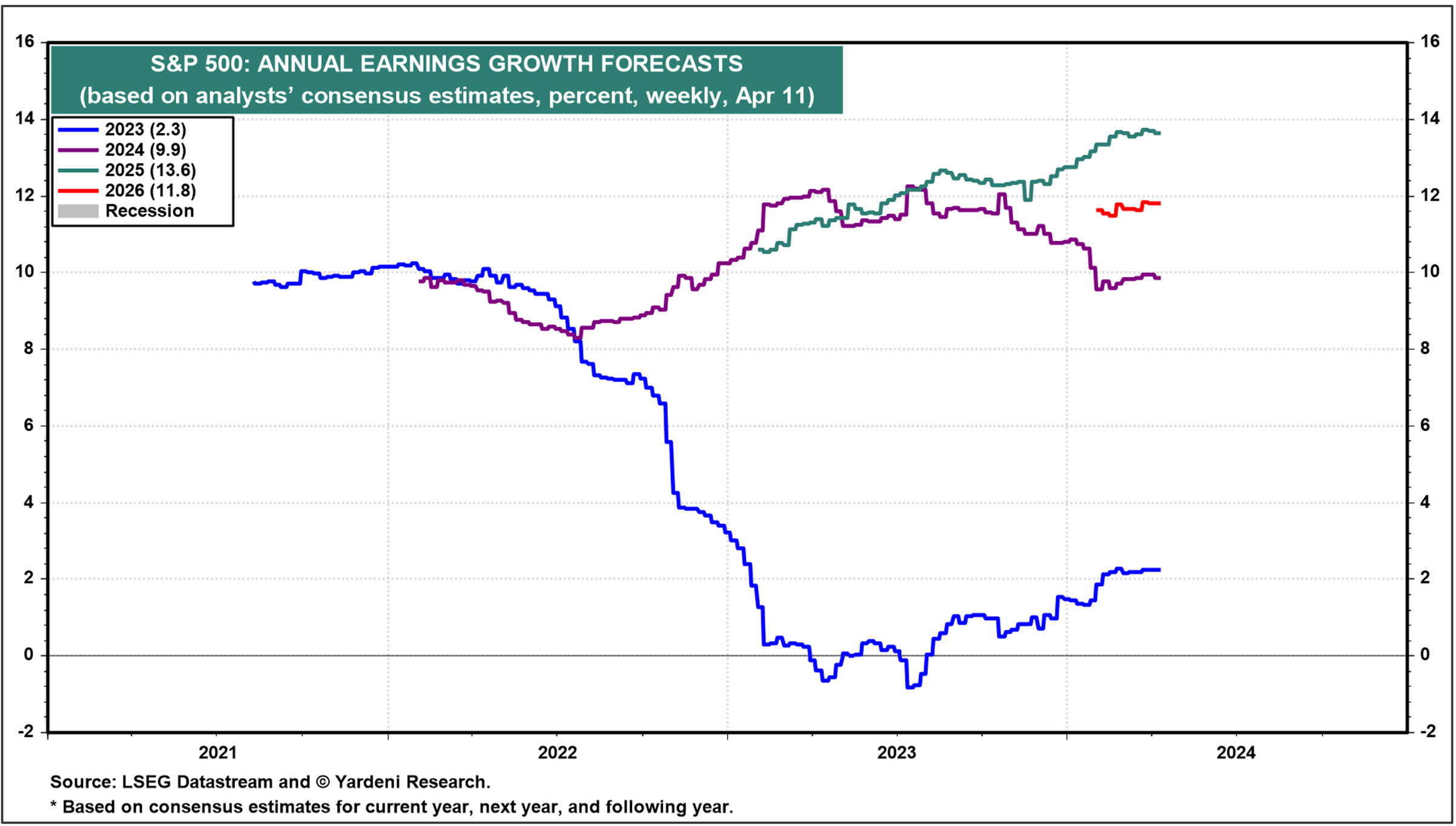

Looking further into the year, the Street expects earnings to be up in the low double digits this year (purple line) and next (teal line – see chart below). If stocks are to renew their upward climb, this is a bogie that has to be met. Valuations are relatively high, high earnings growth rates will be critical to maintain any momentum in equity markets.

After the swift run-up we’ve had, our preference would be to at least pause here, if not have a small correction. Markets that move straight up (or down) are prone to quick reversals. A small correction here would be constructive, not destructive.

Have a great week!

What We’re Reading

Dow tanks 500 points in biggest sell-off of 2024 as JPMorgan slides and inflation fears flare up

Gold surges as Middle East tensions spur safe-haven rush

Visualizing America’s Shortage of Affordable Homes

Biden’s Green-Energy Price Shock

Palumbo Wealth Management (PWM) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where PWM and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.palumbowm.com.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

CPI, Earnings, Inflaction, Interest Rates, PPI, S&P 500, Stock Market, Stocks General NewBy: thinkhouse